Proposed STAR Bond Issuance Policies for the Baseball District Going Before City Council

On February 24, 2010 the City Council approved the addition of the Aces Stadium parcel to the Freight House Tourism Improvement District (the “District”). The City of Reno expects one or more developers will request to enter into reimbursement agreements with the City to use sales tax increment for projects within the District. The information below is a combination of the proposed policies I reported on previously, coupled with recomendations from both the Financial Advisory Board and the Redevelopment Agency Advisory Board, along with examples of how other cities make these kind of deals. John Hester, City of Reno Community Development/Redevelopment Administrator, did an amazing job writing this up in the staff reports, which you can find a link to in the right-hand column.. Use the tabs below to navigate the various sections.

Star Bond Policies for Baseball District

Funding History / Developer Contributions...

The chart below explains the net cost to the developer thus far, and the reimbursements to SK Baseball over time from the city. Because this was a 'catalyst' project, the city is reimbursing SK Baseball for 70% to 110% of the cost to build the baseball stadium (Phase 1A) and subsequent restaurants and bars attached (Phase 2a) . Land provided by both Agency and developer excluded, carrying costs for any developer funds or loans secured by developer excluded; operating profit from stadium and restaurants excluded.

|

Project Phases and Funds/Resources Provided

|

Net Cost to Developer

|

General Notes

|

| Phase 1 Construction Cost: Stadium | $60 million | Construction cost pending final audit |

| Phase 2A Construction Cost: Restaurants | $12 million | Estimated construction cost provided by developer on 1.6.10 pending final audit |

| TOTAL | $72 million | COUNCIL POLICY STATEMENT: DEVELOPER ALLOWED TO RECOVER 100% OF THESE COSTS FROM PHASES 1 & 2A AS THIS IS A CATALYST PROJECT |

| Subtract: $30 million Car Rental Tax Proceeds |

Developer's New Net Cost: $42 million |

|

| Subtract: $20 million Minimum Property Tax Increment |

Developer's New Net Cost: $22 million |

$1 million/year minimum |

| Subtract: Up to $28.5 million Potential Additional Property Tax Increment | Developer's New Net Cost: Ranges from -$6 million Up to $6.5 million) | Maximum additional up to $1.5 million/year for 19 years; FY 10/11 increment will not exceed $1 million |

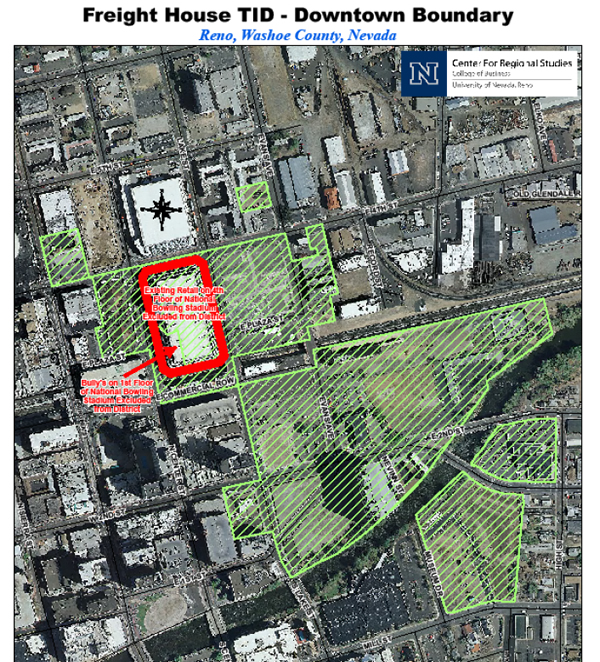

Freight House STAR Bonds District Map

Any future projects within the green highlighted areas below would be eligible for STAR Bonds funding on a first-come, first serve basis. The property highlighted in green below is NOT all owned by the same entity.

STAR Bond Policies

Below is a chart with brief explanations of each proposed STAR Bond Policy, along with recommendations/additions from both the Redevelopment Agency Advisory Board (RAAB) and the Financial Advisory Board (FAB).

| Policy Number | Staff Recommendation | RAAB Recommendation | FAB Recommendation |

|---|---|---|---|

| 1 | No additional public funds (i.e., sales tax increment) for Catalyst Project (Phases 1 and 2A) except per Policy 4. | Same as staff. | Same as staff and RAAB. |

| 2 |

Maximum percentage reimbursement of total project cost for any project: less than 100% Maximum percentage of total revenues from the District to any single project in any given year: less than 100% Maximum total project cost and total revenues in balance. |

Use 25% as maximum percentages; add 25% of the total revenue generated in the District in any single year used for single year projects. | Same as RAAB. |

| 3 | First come, first served; later project reimbursements subordinate to earlier project reimbursements; reimbursement only after fully completed. | Same as staff. | Add ranking of projects. |

| 4 | Sales tax increment funds not used for new projects in any year can be: a.) substituted on a dollar for dollar basis for property tax increment funds for Catalyst Project thus making the property tax increment funds available for other projects at the discretion of the City/Agency, and/or b.) used to repay the interfund loan for Citicenter. | Add c.) used to fund any School District projects in the Freight House District; and add that when the Freight House Sales Tax Increment District is “sunsetted” any uncommitted funds will be used for School District projects in the Freight House District. | Same as RAAB. |

| 5 | None. | Preference given to new projects that: a.) are locally owned (length of time business established in Northern Nevada), b.) local labor (contractor), c.) diversity of use, d.) new business to the City, and e.) higher percentage of private equity. | Add f.) if market outside of the area. |

| 6 | None. | Minimum of 25% private (developer) equity. | Same as RAAB. |

| 7 | None | Reporting on percentage of retail sales from out of state. | Same as RAAB. |

| 8 | None | None | Update “preponderance” report before any new agreements. |

Star Bond Policies, Full Explanation of Each Policy

Policy 1: Freight House District Catalyst Project Funding Levels and Sources:

The original and amended deal between the City of Reno and SK Baseball provided for public reimbursement of 70% to 110% of the pre-audit construction costs for the stadium (phase 1) and the attached restaurants currently under construction and opening this season. Considered a generous subsidy when compared to many other stadium projects in the United States, the City Council approved it because it was a catalyst project for a very run-down section of downtown, the project was being completed during a recession, and that private funding was extremely difficult to obtain at the time. City staff will recommend to the City Council that no additional public funds be provided to the developer for costs associated with the stadium or restaurant complex currently under construction with the exception of Policy 4.

The RAAB strongly supports this staff recommendation and approved a separate motion to unanimously recommend it to the Agency Board. The FAB also supports this recommendation.

Policy 2: Other Freight House District Project Funding Levels and Sources

It's was recommended that future projects in the Freight House District that can benefit from the baseball stadium be eligible for a maximum percentage (i.e., less than 100%) of the project construction costs as a development incentive. There are three components to this policy:

a. No more than a maximum percentage of the total project costs may be reimbursed using sales tax increment funds;

b. No more than a maximum percentage of the total sales tax increment generated in the Freight House District in any single year may be used for reimbursing any single project; and

c. If the sum of the reimbursements for all projects with a reimbursement of total project costs exceeds the total sales tax increment in any one year, then the reimbursement for the most recently approved project(s) will be reduced until the total increment and the individual project reimbursements are in balance. The rationale for this recommendation was that the catalyst project has already been completed and should generate demand for multiple additional projects that do not require 100% subsidy. Hence, no single project should obtain more than a maximum percent of the sales tax increment funds. Additionally, the flow of funds to subsidize new projects should be made available to multiple projects in any given year so multiple projects can be implemented in any given year. Hence, no project could receive a subsidy of more than a maximum percentage of the total funds generated in the district in any single year.

In general, a smaller project would receive a larger percentage of project cost subsidy per year over a shorter period of time while a larger project would receive a smaller percentage of project cost subsidy per year over a longer period of time. This would allow for a mix of both large and small projects over varying time frames. A disposition and development agreement for each specific project must be in place to utilize this funding source.

The RAAB recommended the maximum percentage of project costs and the maximum percentage of total revenue generated in the District in any single year that can be used for a single project be set at 25%. The RAAB also recommended that 25% of the total revenue generated in the District in any single year be used for single year projects. The FAB recommended this policy as refined by the RAAB.

Policy 3: Priority of Funding Commitments for Other Freight House District Projects

The intent of this policy recommendation was to create a funding environment in which all property owners in the Freight House District are able to make project proposals, and to reward those that move the fastest in completing their projects and redeveloping the District. Additionally, funding is not provided until the project is fully completed versus the City/Agency issuing bonds prospectively and the developer being required to provide private financial guarantees to ensure completion (e.g., surety bonds, etc.).

The policy has three components:

a. The first project proposed will be the first considered (i.e., “first come, first served”);

b. Funding commitments for later projects will be subordinate to earlier projects; and

c. Funding will be provided only on a reimbursement basis when the project is fully completed in accord with the funding agreement and any applicable approval conditions and regulations (i.e., all expenditures are audited, all conditions of approval must be met, the project must have a permanent certificate of occupancy, etc.). This does not guarantee the provision of bond funded reimbursements, as the type of reimbursement must be determined based on the City’s overall financial position.

The RAAB recommended this policy as proposed by staff. The FAB recommended this policy with the addition of ranking of proposed projects vs. accepting them solely on the timing of the proposal. The FAB also discussed the possibility of the City/Agency soliciting competing proposals and awarding funds to those with the highest ranking, but decided not to make procedural recommendations.

Policy 4: Use of Uncommitted Sales Tax Increment Funds to Satisfy Existing Baseball Stadium Project Funding Commitments

When all of the sales tax increment funds generated in the Freight House District are not committed to other Freight House District projects, they can be used to meet the property tax increment funding requirements for the catalyst project. This will allow projects in other parts of Redevelopment Project Area 1 and Project Area 2 to use the property tax increment funds that would otherwise have to be committed to the baseball stadium project. Specifically, the uncommitted funds would be used at the sole discretion of the City/Agency for the following purposes:

a. Substitute on a dollar for dollar basis for the property tax increment funds to be paid to SK Baseball/Nevada Land per the Amended and Restated Payment Agreement (“ARPA”) thus making the property tax increment funds available for other projects at the discretion of the City/Agency; and/or 77 1

b. Repayment of the inter-fund loan used to purchase the RTC Citicenter site and buildings for future Freight House District development. In addition it is possible for the City to use sales tax increment funds for public projects not listed above. This could be implemented is by creating an agreement to provide the sales tax increment funds to the Redevelopment Agency, which would then disburse the funds for public and/or private projects.

The RAAB recommended adding a third option for uncommitted funding. Specifically they recommended that any uncommitted funds at the end of any year be committed to school projects in the district and that any uncommitted funds available when the District “sunsets” also be committed to school projects in the District. The FAB also recommended this policy as refined by the RAAB.

Policy 5 : Preference of STAR Bond Fund Issuance (added by RAAB)

The RAAB recommended preference be given to projects that meet some or all of the following criteria:

a. The business is locally owned. Locally owned is measured by the length of time that business has been established in Northern Nevada;

b. Local labor and contractors are used for the project construction;

c. The project creates a diversity of use (i.e., not all one type of business)

d. It is a new business to the City (i.e., not relocated from somewhere else within the City limits); and

e. A higher percentage of private equity is provided.

The FAB recommended this policy with an additional criterion: preference be given to projects marketed outside of the area.

Policy 6: Developer Equity (added by RAAB)

The RAAB recommended that a minimum of 25% private (i.e., developer) equity be required. They suggested the other sources of funds could be loans (up to 50%) and the sales tax increment (up to 25%). The FAB also recommended this policy.

Policy 7: Reporting on Retail Sales (added by RAAB)

The RAAB recommended that reporting on the percentage of retail sales from out of state be required. They suggested that sources of this information could include credit card reports and/or point of sale surveys. The FAB also recommended this policy.

Policy 8: Update Preponderance Report

The FAB recommended that the “preponderance” report required for formation of the District be updated before any new agreements are approved. I tend to agree, the preponderance report by Meridian Business Advisers seems to be a bit off-base considering Reno's current economic climate.

How Other Cities / States Do It, and Sample Projects

Whether you are for it or against it, most cities and states in the country utilize some sort of public funding mechanisms to engage in private/public partnerships. Here are some examples of how other states do it, pulled from the City of Reno's staff report:

Project funding policies and practices can be divided into three general categories: gap funding, minimum applicant funding, and rating systems with points based on multiple factors. In some cases these policies and practices are prescribed in state law (e.g., Minnesota). A number of jurisdictions have a hybrid approach using policies and procedures from two or three categories.

Gap Funding: This is also known as the “but for” policy. It essentially states that the developer must demonstrate that the project is not financially feasible “but for” the use of tax increment funds. With this type of funding developers usually have to provide detailed information including at a minimum their financial resources, past development experience, credit history, the proposed project pro forma, information from a private lender on what financing will be provided, etc. and pay for an independent third party to analyze the information. Should the project be approved, the jurisdiction then provides funding for the “gap” amount. Examples of jurisdictions that use this approach are San Diego (Centre City Development Corporation) and several Minnesota jurisdictions.

Minimum Applicant Funding: In this case the applicant or developer must provide a minimum amount of equity funding and financial assurances. Cobb County, Georgia (Atlanta area) requires applicants to provide equity of at least 15% of the total project cost. In Cincinnati, Ohio the developer must provide equity of at least 15% percent of the total project cost and proof of private financing or a completion guarantee surety bond before the city will commit to the project. Lawrence, Kansas states that projects with “at least 50% of total project costs paid by the applicant will be viewed more favorably”.

Rating Systems: Rating systems are used to rank applications based on different criteria. Typical criteria include ratio of private to public funding (e.g., a 5:1 ratio receives 5 points, a 3:1 ratio receives 3 points, a 1:1 ratio receives 1 point), number of full time equivalent jobs created, wage rates, etc. Depending on the total points scored by an application, the project can be approved or rejected, or the project can receive more funding than a project with a lower score. A number of Minnesota jurisdictions, for example, use this approach. Jurisdictions in North Carolina require fiscal and, in some cases, environmental impact analyses. The Government Finance Officers Association recommends that jurisdictions conduct public hearings on proposed projects to gauge community support.

Examples of public/private projects funded:

| Stadium District/ Stadium Projects | Public Funding | Other Funding | Total Funding | Notes |

|---|---|---|---|---|

| Metropolitan Area Projects (MAPS) Phases 1 and 2 Oklahoma City, OK | $363 million | $2.08 billion | $2.44 billion | MAPS utilizes voter approved sales tax with “sunset” provision. Phase 1 and 2 taxes have “sunsetted”. Phase 3 was recently approved by voters and is expected to generate over $700 million in sales tax revenues, however both public and private projects have not yet been built and no total figures for “Other Funding” are available at this point. |

| Cowboys Stadium Arlington, TX | $325 million | $795 million | $1.12 billion | Public funding was provided by a voter approved sales tax. |

| Yankee Stadium New York, NY | $200 million | $1.1 billion | $1.3 billion | $200 million is “minimum” figure. |

Pretty fascinating stuff. While some people might fudge at the high public contribution, this city needs everything it can right now to survive.